A robust credit risk management process is systematic and repeatable. It should cover policy, assessment, risk-based decision making, documentation, and monitoring.

1. Develop a clear credit policy

Set rules for lending decisions, credit limits, and acceptable risk levels. Define risk tolerance, target markets, standard terms, and escalation procedures.

2. Conduct a detailed credit assessment

Run a structured credit risk assessment that includes quantitative and qualitative checks. Review financial statements, credit history, cash flow stability, and market conditions. Evaluate customer concentration and industry risks, and ensure the assessment feeds into broader credit risk analysis frameworks.

3. Make a disciplined credit decision

Use the assessment findings to decide how much credit to extend and on what terms. Align interest rates, collateral requirements, and repayment timelines to the risk profile.

4. Strengthen credit administration and documentation

Ensure loan and credit agreements are complete, enforceable, and compliant. Clear documentation protects the business during disputes and supports audit readiness.

5. Monitor the borrower continuously

Set up ongoing credit risk monitoring to detect early warning signs. Track payment behaviour, compliance with covenants, cash flow movements, and external market developments.

6. Prepare for remediation and collections

Create structured steps for early intervention, restructuring, and recovery. Use defined reminders, negotiation protocols, and legal pathways to minimize loss and resolve overdue accounts quickly.

You can also read: The CFO’s Playbook for AI-Ready Finance Teams

Select an element to maximize. Press ESC to cancel.

Select an element to maximize. Press ESC to cancel.

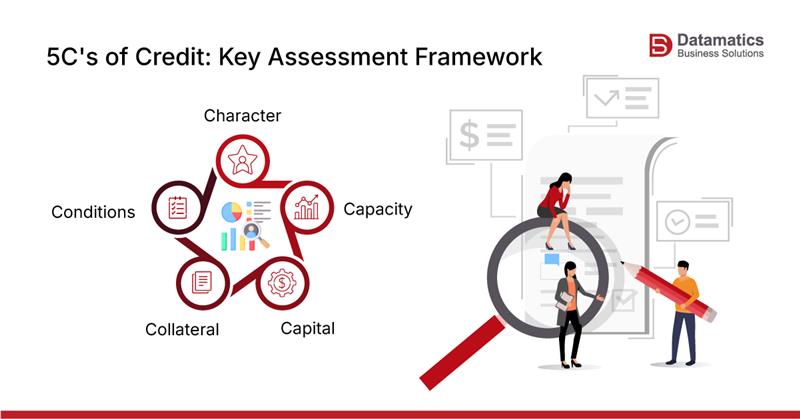

The Five Cs of Credit give CFOs a clear, consistent framework for evaluating borrower quality. They help teams build stronger credit scoring models, improve portfolio risk analysis, and make lending or trade credit decisions that align with the organization’s risk tolerance. Here’s what it entails:

Character

Assesses the borrower’s reliability and repayment behaviour by reviewing credit reports, past delinquencies, dispute patterns, and financial discipline.

This matters because a borrower with poor payment behaviour increases operational effort, disrupts cash flow, and raises the likelihood of default.

Capacity

Measures the borrower’s ability to meet repayment obligations by analyzing cash flow, liquidity ratios, debt levels, and existing commitments.

This is crucial because even well-intentioned borrowers default if they lack the financial capacity to repay, and early signs of strain often appear in these metrics.

Capital

Evaluates how much the borrower has invested in the business or transaction.

This matters because higher internal investment signals commitment, lowers credit risk, and shows that the borrower is willing to share financial responsibility instead of shifting it fully to the lender.

Collateral

Identifies assets available to secure the exposure and improve recovery prospects if default occurs. This matters because secured credit significantly reduces potential loss and enables lenders to extend credit in situations where unsecured lending would be too risky.

Conditions

Considers macroeconomic trends, industry performance, competitive pressures, and regulatory factors. This matters because even a strong borrower can struggle if external conditions deteriorate, and forecasting these risks supports proactive credit exposure management.

You can also read: How CFOs Can Drive Growth in 2026 with Smart SaaS Accounting Outsourcing